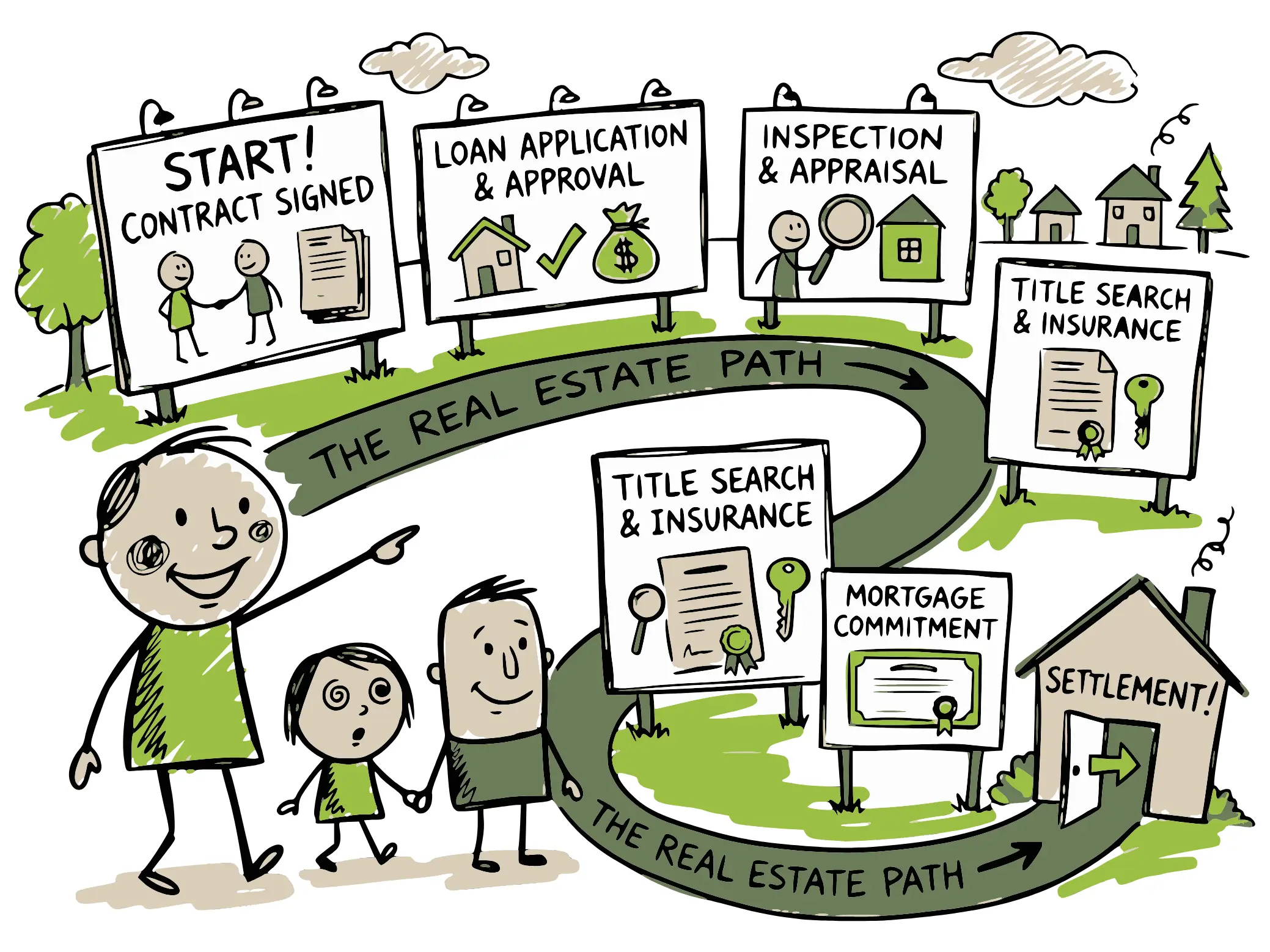

The offer got accepted. Congratulations, and welcome to the part of the transaction nobody explains at the open house. Between a fully signed agreement of sale and settlement day sits a stretch of roughly 30 to 60 days with its own rhythm: a busy first two weeks, a quiet middle where the lender and title company do their work, and a fast finish.

If you want the full journey from "thinking about it" to keys in hand, my Buyer's Guide lays out all 13 steps. This post zooms in on the six or so weeks in the middle that the guide calls execution, contingencies and the home stretch.

The clock starts the day everyone signs

Under contract means the agreement of sale has been signed by both sides. From that moment, the dates inside it are binding. Pennsylvania's standard agreement says so explicitly, and missing a performance date can cost you rights you thought you had. I wrote more about that in when it's okay to walk away from a deal, but the short version is that the calendar is the contract.

The first few days are administrative and quick:

- The deposit moves. Your earnest money goes into an escrow account, usually held by the listing broker or the title company. It sits there until settlement, when it's credited back toward what you owe.

- Inspections get scheduled. The inspection window is short, so a good agent has the inspector lined up almost immediately.

- The mortgage application goes in. A pre-approval got you to the table; now the lender needs the formal application tied to this specific property.

- Title gets ordered. The title company starts researching the chain of ownership so any problems surface early, while there's still time to fix them.

Weeks one and two: the inspection window

In a typical Pennsylvania deal, the buyer has a negotiated window, commonly 10 days, to complete inspections and deliver reports, followed by a negotiation period for working through whatever turned up. What each inspection actually covers gets its own post, because in this housing stock the add-ons matter: a sewer scope on an older lateral, radon in a finished basement, a specialist's eye on an original slate roof.

The negotiation that follows is the emotional center of the whole under-contract period. It ends in repairs, credits, a price adjustment, or a handshake and a clean pass. Sometimes the answer is that buyer and seller can't bridge the gap, and the buyer exits with the deposit. That's the contingency doing its job. Most of the time, both sides land somewhere reasonable and the deal keeps moving.

The quiet middle: financing and title

Once inspections resolve, the file goes underground for a few weeks. This part feels like nothing is happening. In reality, two teams are working in parallel.

The lender is underwriting. The appraisal gets ordered, your finances get verified, and somewhere in there the underwriter asks for a document you're certain you already sent. Send it again, quickly. The agreement's mortgage commitment date is a hard deadline, and if it passes without a formal commitment, the seller may gain the right to terminate. I covered how commitment timing plays into offer strategy in cash vs. financed offers. Respond to your lender the same day, every time.

The title company is searching. In Northwest Philadelphia and eastern Montgomery County, homes have long histories: estates, subdivisions, liens paid off decades ago and never properly recorded. The title search finds these, and the seller is obligated to deliver good and marketable title. Most issues are curable with paperwork and time, which is exactly why title gets ordered in week one and not week five. The closing-costs post covers what the title policy costs and why I consider the owner's policy close to essential in 80-to-140-year-old housing stock.

One number for reassurance while you wait: ICE Mortgage Technology's origination data puts the average time to close a purchase loan at about 42 days. If your timeline is quiet in week four, you are on schedule, not stuck.

If you're the seller, this stretch has its own checklist

Sellers aren't just waiting. This window is for completing any repairs you agreed to in the inspection negotiation (keep receipts; buyers will want them at the walkthrough), lining up your own move, confirming your mortgage payoff figures and handling any municipal requirements. Some townships around here require a use-and-occupancy or resale certification before settlement, and the lead time varies by municipality, so it belongs on the week-one list rather than the week-five one.

The Seller's Guide covers the full arc from pricing to closing day. The part that matters most in this stretch: the house needs to be in the condition the contract promises, empty except for what the agreement says stays, by the time the buyer walks through.

The last week: walkthrough, numbers, keys

A few days out, three things converge:

- The closing disclosure arrives. For financed buyers, the lender must deliver the final numbers at least three business days before settlement. Compare it against your loan estimate and ask about anything that moved.

- The final walkthrough happens. Usually within a day or two of settlement. You're confirming the home is as the contract promised: repairs done, systems working, nothing newly broken, nothing missing. It's verification, not a second inspection, and it's the right moment to raise a problem, because leverage drops sharply after you sign.

- Settlement day. Everyone signs, funds transfer, the deed gets recorded and the keys change hands. Bring photo ID and any funds due as a wire or certified check per your title company's instructions. Plan for about an hour at the table.

When something wobbles

Deals hit turbulence, and it helps to know the base rates. In NAR's most recent REALTORS® Confidence Index survey, about 6 percent of contracts were terminated over the prior three months, and about 13 percent had a delayed settlement. Read those numbers the other way: the overwhelming majority of contracts close, and most problems resolve as delays, not deaths. Appraisal gaps get negotiated, underwriting conditions get cleared, settlement dates get pushed a week by mutual agreement.

The pattern I see in the deals that go smoothly is boring and repeatable. The buyer responds to the lender fast, both agents watch the dates, and nobody lets a small problem age into a big one. If you're heading under contract on a home in Northwest Philadelphia or Montgomery County and want someone watching those dates with you, reach out. This stretch is much calmer with a map.

I'm a REALTOR®, not a lawyer or a lender. Timelines and contingency windows are set by your specific agreement of sale, and the provisions referenced here come from the Pennsylvania Association of Realtors standard forms. Consult your agent and, where appropriate, a licensed Pennsylvania real estate attorney about your transaction.

Sources: National Association of REALTORS®: REALTORS® Confidence Index, ICE Mortgage Technology: Origination Data Reports.

Henry is a Philadelphia-based REALTOR® serving buyers and sellers in Northwest Philadelphia and Montgomery County, PA. Questions? Get in touch.

Frequently Asked Questions

How long does it take to close on a house after the offer is accepted?

For a financed purchase in Pennsylvania, plan on roughly 30 to 60 days between a fully signed agreement of sale and settlement day. ICE Mortgage Technology's origination data puts the national average time to close a purchase loan at about 42 days. Cash purchases can settle much faster, sometimes within a couple of weeks, because there is no lender underwriting or appraisal in the way. The actual settlement date is negotiated in the agreement itself.

What happens right after both parties sign the agreement of sale?

The moment the agreement is fully executed, you are under contract and every performance date in the document becomes binding. Within the first few days the buyer's deposit goes into escrow, inspections get scheduled, the formal mortgage application goes in and the title company is engaged to start its search. The early days are the busiest part of the whole under-contract period.

What is a mortgage commitment date?

It is the deadline written into the Pennsylvania agreement of sale by which the buyer must deliver the lender's formal, underwritten approval of the loan. A commitment is a step beyond pre-approval. If the date passes without one, the seller may gain the right to terminate, so buyers should respond quickly whenever the lender requests documents and ask for a realistic commitment window up front.

What should buyers check at the final walkthrough?

The walkthrough, held shortly before settlement, confirms the home is in the condition the contract promised. Check that agreed repairs are complete, systems and fixtures still work, nothing was damaged in the move-out and nothing the contract says stays has disappeared. It is a verification visit, not a second inspection, and problems found there are raised before you sign, not after.

How often do home sales fall apart between agreement and closing?

Less often than buyers fear. In NAR's most recent Confidence Index survey, about 6 percent of contracts were terminated over the prior three months, and about 13 percent had a delayed settlement. Most deals close, and most of the ones that wobble are delayed rather than dead, usually over financing, appraisal or repair logistics.